How do you pay for a kitchen renovation when your savings account isn’t quite ready for the hit?

Most homeowners eventually find themselves staring at a cracked countertop or a leaking roof, realizing that their bank balance and their ambitions are at a standoff. It’s the classic dilemma: you want the granite, but you also want to keep your retirement funds intact. This is where the personal loan enters the conversation, acting as a bridge between a dilapidated living room and a finished basement.

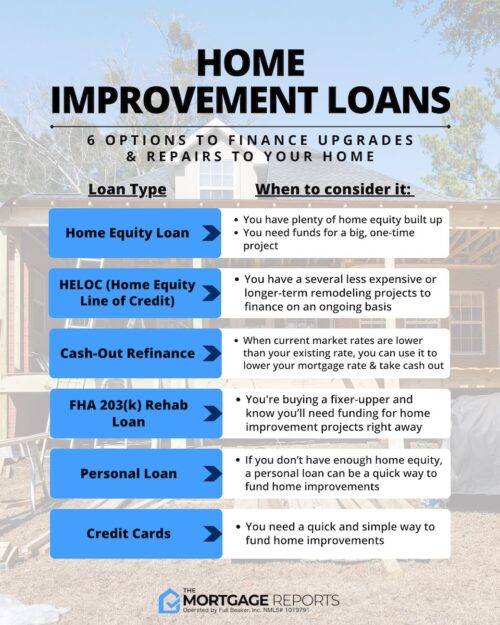

Financing a renovation isn’t one-size-fits-all. You can tap into your equity, use a credit card, or grab an unsecured personal loan. Each path has its own rules, interest rates, and fine print that can either save your budget or sink your credit score if you aren’t paying attention. Understanding these products is the difference between a smooth renovation and a financial headache that lasts longer than the construction itself.

The Cost of Speed and the Interest Gap

When you look at the math, the distinction between loan types is clear. If you take out a home equity loan, the interest you pay might be tax-deductible because the money is tied directly to the asset. A personal loan doesn’t get that same luxury. According to NerdWallet, interest paid on a personal loan is not tax-deductible, which is a significant factor to calculate when you are crunching the numbers for a large-scale remodel.

The rates themselves are a moving target. Currently, home improvement loan rates range from about 7% to 36%. If you have a credit score that looks like a high-performance stock ticker, you might land on the lower end. If your credit is less than stellar, you might find yourself paying double digits that make the project significantly more expensive than the initial contractor quote suggested.

Speed is the real selling point here. Some lenders, like Wells Fargo, offer a same-day credit decision for most customers who apply. This helps when a contractor is standing in your kitchen, hammer in hand, asking when the check is going to clear. You aren’t waiting weeks for an appraiser to visit your property. You just need the funds to cover materials or labor.

Comparing the Interest Landscape

It helps to visualize how these costs shake out. While a credit card might offer a quick fix, the compounding interest can be a nightmare. A personal loan offers fixed terms, which provides a sense of certainty that a revolving line of credit lacks.

| Financing Type | Collateral Required | Typical Interest Rate | Tax Deductibility |

| Home Equity Loan | Yes (Your House) | Lower | Often Yes |

| Personal Loan | No | Higher | No |

| Credit Card | No | Highest | No |

Choosing the right path requires a cold-eyed look at your long-term debt capacity. If the project is a quick fix like a leaky faucet or a new backsplash, a small personal loan or even a line of credit might suffice. If you are building a whole new wing, you’re looking at a much larger financial undertaking.

The Scope of Use and Project Limits

What can you actually do with this money? The beauty of a personal loan is its versatility. Most lenders don’t care if you are paying a professional crew or buying rolls of hardwood flooring from a local warehouse. You aren’t restricted to “permitted” improvements the way a government-backed loan might dictate.

You can use personal loans for home improvement projects such as a new addition, a pool, or other renovations. This versatility makes them a favorite for those who want to add value to their property without the hassle of a mortgage-linked product. Using a personal loan for home renovations could be a smart way to upgrade or add value to your home without increasing your mortgage, avoiding the hassle of the equity process. This keeps your primary lender out of your business, which many homeowners prefer.

But don’t assume every lender is equally flexible. While some banks want to see a detailed breakdown of your contractor estimates, others are happy to just hand over the cash. Some specialized lenders even offer options for those who need a bit more flexibility in their repayment schedule, such as installment loans or lines of credit. If you are searching for specific terms, you might find that texasloanstoday.com provides different avenues for managing these costs.

It is worth noting that not every project justifies a large loan. Some people try to over-borrow for minor aesthetic changes. If you only need five thousand dollars for new lighting fixtures, taking out a massive personal loan with a three-year term might be overkill. Always match the loan’s term to the project’s lifespan. You don’t want to be paying off a new dishwasher for five years.

When to Choose a Line of Credit

A line of credit is a different animal entirely. Instead of getting a lump sum, you get access to a pool of funds. You only pay interest on what you actually spend. This is ideal for phased renovations where you might need money for the demolition this month, but won’t need the tiling funds until three months from now.

It prevents you from paying interest on money that is just sitting in your checking account. It is a surgical approach to financing. However, it requires more discipline. It is very easy to treat a line of credit like a piggy bank for things that aren’t home improvements.

Navigating the Credit and Approval Maze

The approval process is where the optimism of a DIY enthusiast meets the cold reality of a bank’s risk department. Lenders want to know one thing: will you pay them back? They look at your debt-to-income ratio, your employment history, and most importantly, your credit score. This is why the rate spread is so wide. A difference of fifty points on your credit score can literally cost you thousands of dollars over the life of the loan.

But what if your credit isn’t perfect? There are options, though they come with caveats. Some lenders specialize in providing solutions for smaller repairs or renovations even if your financial situation isn’t pristine. You might find yourself looking at payday loans or installment loans from companies like Advance America. These can be quick, but the interest rates can be predatory if you aren’t careful. Always read the fine print regarding the total cost of credit.

And don’t forget about the fees. Some lenders will offer a great rate but then hit you with an origination fee. This is an upfront charge that is often taken directly out of your loan proceeds. If you borrow $10,000 but the lender takes a $500 origination fee, you only get $9,500. You need to account for this when you are calculating whether you have enough to finish the job. It’s a small detail that ruins many a budget.

It is a game of math. If you’re looking for a quick and reliable way to finance your home improvement project, you might want to explore the loan options available at Advance America. They offer multiple solutions, including Payday Loans, Installment Loans, and personal Lines of Credit. Depending on your financial situation, you may qualify for various products that cater to different levels of creditworthiness.

Comparing Loan Providers and Terms

Not all banks are created equal. Some are massive institutions that prioritize stability and low rates for their best customers, while others are more agile and willing to take a chance on a borrower with a slightly bruised credit history. You have to decide whether you want the prestige of a big-name bank or the accessibility of a specialized lender.

When you’re shopping around, don’t just look at the monthly payment. The monthly payment is a trap if it’s low because the term is long. A 72-month loan might have a tiny monthly payment, but you’ll end up paying for that kitchen until your kids are in college. Always look at the total interest paid over the life of the loan. That is the real number that matters. That is what’s actually leaving your wallet.

Comparing rates and terms is essential. As The Wall Street Journal suggests, you should cover home improvement projects with personal loans, credit cards, or home equity financing, but you must compare rates and terms to get the best deal. A credit card might have a 0% introductory APR, which is tempting, but if you don’t pay it off before the promo ends, the interest rate will skyrocket, making your new deck much more expensive than you planned.

It’s a balancing act. You are balancing the urgency of the repair against the long-term cost of the debt. You are balancing the security of your home against the convenience of an unsecured loan. There is no perfect answer, only the answer that fits your specific spreadsheet.

Check the total cost of borrowing before signing anything.

Good to know

Can I get a personal loan for home improvement with bad credit?

Yes, many lenders offer personal loans for bad credit, though you may encounter higher interest rates and lower borrowing limits.

Are there any zero interest home improvement loans available?

While rare, some credit unions offer promotional 0% APR periods, and certain energy-efficient upgrades may qualify for specialized low-interest financing.

What are the differences between unsecured home improvement loans and traditional loans?

Unsecured home improvement loans do not require your property as collateral, meaning your home is not at risk if you default on payments.

Are there government loans for remodeling a home?

Yes, programs like FHA 203(k) loans allow homeowners to finance renovations by adding the costs to their existing mortgage.

How do home improvement loan rates work?

Rates are determined by your credit score, debt-to-income ratio, and the loan amount, with better credit typically securing the lowest interest rates.

0 Comments